You might have heard of the Registered Retirement Income Fund (RRIF), but have you heard of its cousin, the Life Income Fund (LIF)? Like most relatives, they’re connected in fundamental ways—they both pay out income in retirement—but their backgrounds are quite different. Here’s what you need to know about LIFs.

What is a LIF?

A LIF is what a Locked-in Retirement Account (LIRA) eventually gets converted into in retirement, similar to how a Registered Retirement Savings Plan (RRSP) gets turned into a RRIF.

We’ve written about LIRAs before, and it’s a good idea to familiarize yourself with that type of account, but essentially it’s only for funds that were once invested in an employer-sponsored pension plan. You might have a LIRA because you left one job for another, and instead of keeping the money with your employer, you chose to take the commuted or lumpsum value of the pension account and move it to the financial institution of your choosing.

A LIRA is like an RRSP, only you can’t add money to it or withdraw funds before retirement. You can continue to grow your assets inside of one, though. Eventually you’ll have to convert your LIRA into a LIF, just like you would convert an RRSP into a RRIF.

When do I have to convert my LIRA into a LIF?

Depending on the jurisdiction of the account, (some provinces have age requirements to start withdrawals), you can begin accessing income from your LIRA by converting it to a LIF. For example, in Alberta and B.C. you need to be aged 50, whereas New Brunswick doesn’t have an age requirement. However, in the year you turn 71, you will have to convert your account into a LIF and start withdrawing funds from it. Some provinces also require you to convert your LIF to a life annuity when you turn 80.

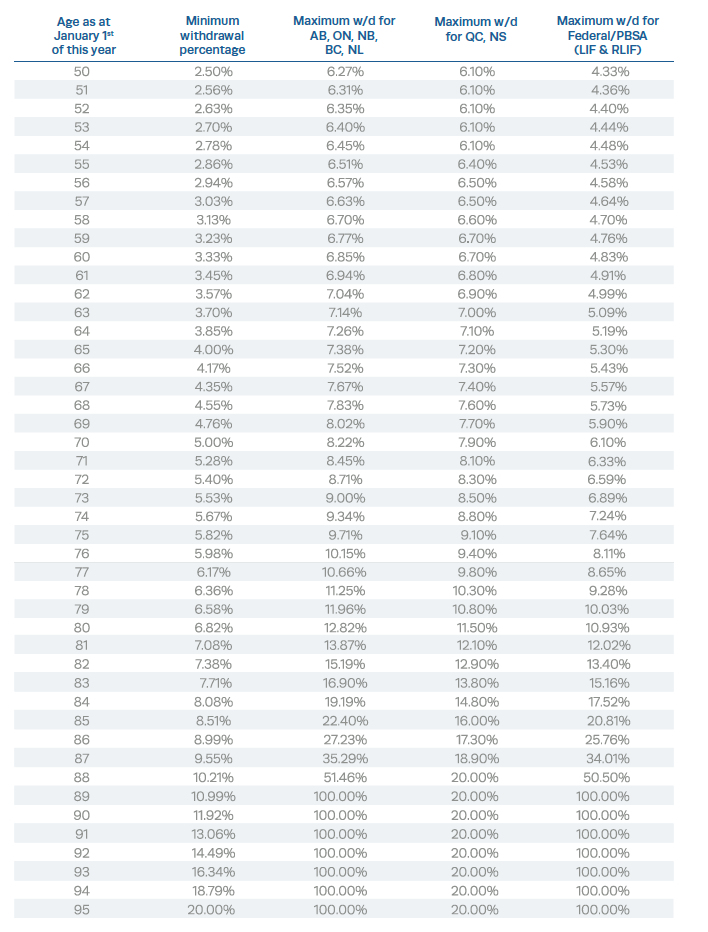

How much can I withdraw?

Unlike a RRIF, you’re not allowed to withdraw the entire amount from a LIF in a lump sum. The account has a minimum and maximum withdrawal amount, which is a percentage of the account total that shifts according to your age. The table below shows the minimum and maximum withdrawal percentages for LIF accounts in 2022 by province. Depending on your age or in some cases your spouse’s age, you must withdraw an amount as outlined by the percentages below.

NOTE:

Quebec, Alberta, New Brunswick, and British Columbia pension legislation permits LIF clients who begin a LIF in the middle of a calendar year with funds transferred from a LIRA or pension plan to take the full maximum payment for the year. First year payments under the other jurisdictions must be prorated based on the number of months the LIF was in force.

ON, BC, AB, NL maximum calculations are based on the greater of a) the result using the factor and b) the previous year’s investment returns. MB LIF maximum calculation is based on the greater of a) the result using the factor and b) the previous year’s investment returns + 6% of the value of all transfers in from a LIRA or Pension Plan during the current year.

Source: Service Canada. Figures updated as of December 2021. Visit servicecanada.gc.ca for updated figures.

The minimum withdrawal is based on the same calculation used for RRIFs, while the maximum withdrawal amount is calculated according to provincial or federal legislation.

You can arrange for annual, semi-annual, quarterly, or monthly payouts as long as the total remains within that minimum-maximum guideline.

How does tax work?

Withdrawals from a LIF count toward your gross annual income on your tax return. Your financial institution will provide you with a T4-RIF for tax purposes, which shows how much you withdrew in the previous year and any tax that might have been withheld.

As is the case with a RRIF, you may choose to name your spouse or other heirs as beneficiaries so that any remaining funds can be transferred to them upon your death, or, you can also choose to designate it to your estate and have it disseminated through your will.

While few people have heard of the LIF, it’s something that those paying into pension plans must understand before moving to a new job. The more you know about how retirement funds work—RRIFs, too, as you may also have RRSP income that will need to one day be withdrawn—the better your retirement will be.