Chris Hanley, CA, CPA, CFP® and Denika Heaton, BBA, JD, TEP, CEA

Mawer Tax and Estate Planning Specialists

With some of the 2024 tax changes from the Federal Budget now in effect, trusts used for income splitting that rely on financing strategies like prescribed rate loans may now face taxes that they weren’t previously subject to.

To help understand how these changes may impact you, we've created a short primer on:

- Prescribed rate loan trusts and their purpose

- AMT changes impacting these trusts, with an example

- Key planning steps for trustees to consider

What is a Prescribed Rate Loan Trust?

A prescribed rate loan trust is a tax-saving strategy that allows Canadians to split income with family members, typically those in lower tax brackets, by lending money to a trust at the prescribed interest rate set by the Canada Revenue Agency (CRA).

The trust then invests this borrowed money to generate income. The trust's income (after paying the prescribed interest rate) is then distributed to the trust’s beneficiaries and taxed in their hands—often at a lower tax rate—or not taxed at all, if the beneficiary’s personal tax credits are sufficient.

Why is This Strategy Used?

By paying interest at the prescribed rate, this strategy avoids tax attribution rules that would otherwise attribute the income back to the high-income lender if they gifted or loaned money directly to the trust or a low-income family member for investment. Additionally, by distributing the net income (after interest costs) to beneficiaries, the trust itself doesn’t have taxable income and therefore doesn’t owe tax.

This strategy was particularly appealing during periods of low interest rates, when the prescribed rate charged to the trust was just 1% or 2% and the rate could be “locked in” for the duration of the arrangement. As long as the trust's investment income exceeded the prescribed interest rate, the excess could be shared with family members in lower tax brackets. However, recent interest rate increases have made this strategy less attractive to implement today1.

What is Alternative Minimum Tax?

Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that individuals and most trusts pay a minimum level of tax, regardless of deductions, exemptions, or credits that might otherwise reduce their tax liability under the regular tax system. The AMT recalculates income tax after adjusting income calculated under the regular tax system.

If the AMT exceeds the regular tax liability, the taxpayer pays the higher amount. But AMT paid is not necessarily lost; it can be credited against regular tax liabilities for the following seven years, if there is sufficient regular tax in those years.

For individuals, there is a basic annual exemption from AMT of $173,205 for 2024 (indexed to inflation), which helps ensure it only applies to individuals with higher incomes. However, this exemption does not apply to trusts.

What AMT Changes Will Affect Prescribed Rate Loan Trusts?

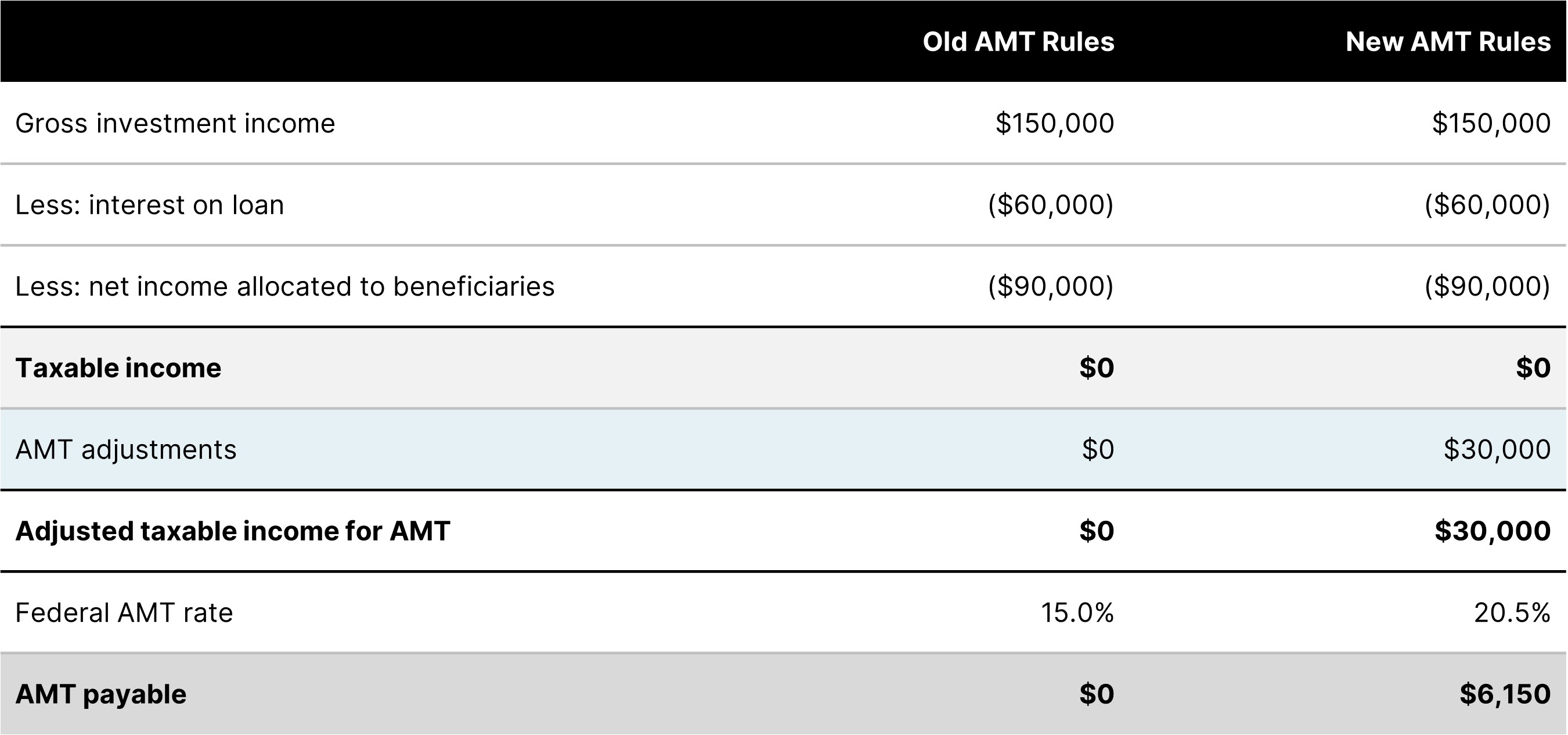

Several changes have been made to AMT (effective January 1, 2024), including increasing the federal AMT rate from 15% to 20.5%. The key change impacting prescribed rate loan trusts is that now only 50% of the interest paid on most investment loans will be deductible (compared to 100% previously) when calculating AMT. This means that even if all trust income is allocated to beneficiaries and the trust has no regular taxable income, it may still be subject to AMT.

Example

An individual lent $3,000,000 to a trust when the prescribed rate was 2%. The trust invested these funds in a portfolio of securities, generating $150,000 in gross investment income annually. The net income is allocated to the individual’s children, who are the beneficiaries of the trust. For simplicity, let’s assume the trust has no other expenses.