What is a RRIF?

A Registered Retirement Income Fund (RRIF) can be thought of as the natural evolution of the Registered Retirement Savings Plan (RRSP). An RRSP is used to save for retirement, whereas the RRIF is used to fund your retirement. Both accounts offer the same investment options, including mutual funds, stocks, bonds, or GICs, which all grow on a tax-deferred basis while inside the account. For additional context, you can also read about the most common misconceptions about RRIFs.

Converting an RRSP to a RRIF

You can convert an RRSP to a RRIF at any age, but no later than the year in which you turn 71. Once an RRSP becomes a RRIF, no further contributions can be made to the account. Your financial institution will be able to help you understand your options and the paperwork needed to make that conversion.

Withdrawals

There is no maximum withdrawal requirement; however, a minimum amount must be withdrawn annually from your RRIF starting in the year after it is opened.

You can choose to receive your withdrawals on a schedule that works for you. This may be weekly, bi-weekly, monthly, semi-monthly, quarterly, semi-annual, or annual.

If you don’t need to use the withdrawn funds, you may decide to reinvest the proceeds into your non-registered account or TFSA, if you have the contribution room.

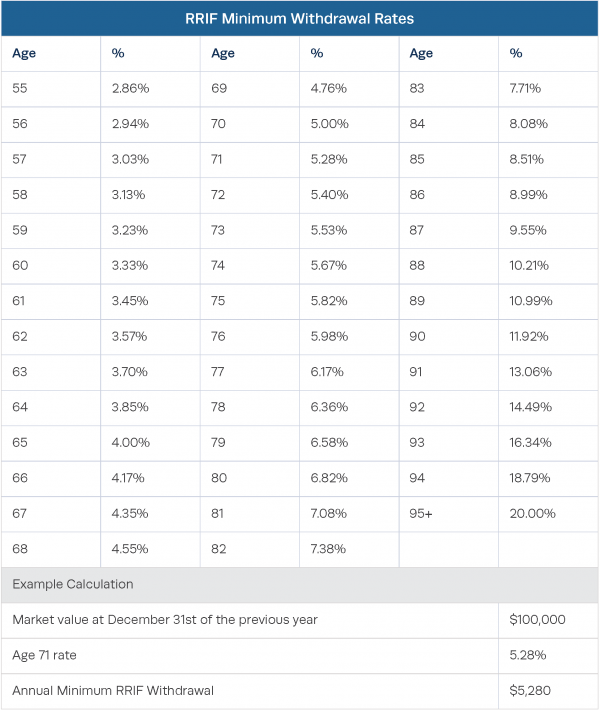

The minimum withdrawal amount is calculated by your account size as of December 31st of the previous year, your age, and the corresponding minimum withdrawal rate (%), as shown below. If your spouse is younger than you, you may choose to reduce the minimum withdrawal amount by basing the calculation on their age rather than your own.

The withdrawal percentages for different ages and an example calculation are shown below.

Tax Treatment

Any withdrawal from a RRIF is considered taxable income in the year received.

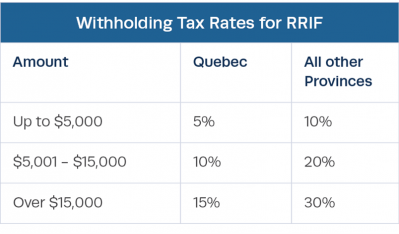

There is no withholding tax on a minimum withdrawal; for amounts over the minimum, however, the following withholding tax rates are automatically applied by your financial institution.

Why you may choose to convert your RRSP into RRIF before turning 71

If you are over the age of 65, withdrawals from a RRIF are considered pension income for tax purposes, while withdrawals from an RRSP are not. So, if you don’t have any other pensionable earnings, converting your RRSP to a RRIF earlier, at age 65, can offer two main benefits:

- The pension income tax credit enables you to deduct a tax credit of your pension income up to a maximum of $2,000 per year.

- Pension income splitting allows a spouse to transfer up to 50% of their eligible pension income to their spouse for tax purposes. This can help to shift some of the tax obligation from the higher income spouse to the lower income spouse (in a lower tax bracket), resulting in less taxation overall.

We recommend speaking to an investment professional to help determine the best course of action.

Designating your beneficiary

You have a few options to choose from when designating your beneficiary.

Successor Annuitant (if you have spouse or common-law partner)

When the RRIF annuitant (holder) dies, the account simply continues under the ownership of the surviving spouse/partner. They receive the payments, and withdrawal amounts remain unchanged. The successor annuitant pays taxes on any withdrawals.

Beneficiary (if you have a spouse or common-law partner)

When the RRIF holder dies, the RRIF is collapsed and the proceeds can be transferred to the surviving spouse’s/partner’s RRIF or RRSP. Taxes are deferred for the deceased’s estate and the surviving spouse/partner until they withdraw the money (once transferred) from their own RRIF or RRSP.

Beneficiary (for a non-spouse)

The value of the account on the date of death would be taxable to the deceased on their final tax return, while the full value of the RRIF goes to the beneficiary. In short, the estate pays the taxes while the beneficiary receives the full account value. Anyone can be named as the beneficiary of a RRIF—including charities.

The decision to appoint a beneficiary or successor annuitant can be nuanced, so we do recommend speaking to an investment professional to help select the best option for you. (Note: beneficiary and successor annuitant designations are unavailable in Quebec.)