President’s message

The start of a new year is always a good time for reflection, and this year perhaps even more so as we move into the next decade. As I think back on the last 10 years, there have been many significant developments from a global perspective: the longest bull market in history; Apple unveiling the first iPad; Trump elected U.S. President (and impeached); the surge of Bitcoin; Twitter, Facebook, and Alibaba going public; unprecedented monetary policy intervention from central banks; Brexit; trade tensions between the U.S and China; protests in Hong Kong; and the list goes on.

From a firm perspective, we have also seen many significant developments over the past decade: we launched three new funds (Global Balanced Fund, Global Bond Fund, and the Emerging Markets Equity Fund); our assets under management increased from $6.7 billion to over $64 billion; the Balanced Fund (Series A) delivered an annualized 10-yr return of 9.3%; we moved office locations in Calgary and established offices in Toronto and Singapore; as a firm we donated over $5 million to communities; and we made the decision to remain an independent firm.

Although the firm has experienced significant change over the past decade, I’m most struck by what has stayed the same—our firm’s core values: act with integrity, put clients’ interests first, pursue excellence, work as a team, and think long-term. It is our continued commitment to these values that has made us the firm we are today and the firm we will be in the future. On behalf of everyone at Mawer, I want to thank you for putting your trust in us. We know that you have a choice of investment managers and we are honoured and humbled by your ongoing support.

We wish you all a very Happy New Year,

Craig Senyk

Market overview

What a stark contrast a year brings. A year ago, in the fourth quarter of 2018, we were in the midst of a sudden, sharp market decline. Interest rates were rising, parts of the yield curve had inverted, and fears of a global recession were rampant. Uncertainty abounded, most notably with respect to the future path of interest rates, U.S./China trade negotiations, and Brexit.

This year, the fourth quarter of 2019 closed with a risk-on rally in which risky assets globally capped off a remarkable comeback. The shift in investor psychology that began in early 2019 with central banks’ recommitment to lower interest rates further improved in Q4 as some of the uncertainty investors had been worried about was removed: negotiations between the U.S. and China appear to be progressing, the Conservatives’ decisive victory in the U.K. gave Brexit clarity, and, closer to home, the results of the Canadian election largely signalled “business as usual.”

Fortunately, we don’t aggressively position portfolios for one particular outcome, but instead view the world in a probabilistic way, remaining mindful that many different outcomes, both positive and negative, may unfold. Looking back a year ago, as the odds worsened, we did shift to a more defensive stance. At the asset mix level, we trimmed equity and increased cash and bonds in our balanced portfolios. Within our various equity funds, we re-allocated capital towards more defensive or resilient businesses. But the magnitude of these changes was modest, and clients were still well- positioned to benefit from a year that unfolded better than most expected. 2019 returns for our balanced funds were solidly double-digit with strong relative returns across numerous asset classes. Investors who went ultra-defensive missed this opportunity.

This isn’t the only way to invest. Others do make more aggressive moves to position for one outcome over another. It’s great when it works. Not great when it fails. Since we don’t believe our edge is to consistently forecast macro events or inflection points in a cycle, we’ll continue to make modest portfolio adjustments as events unfold.

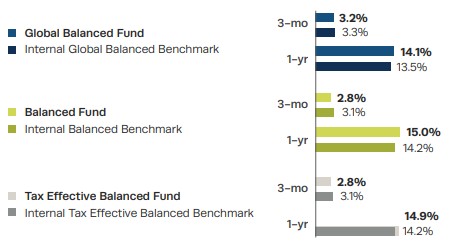

How did we do?

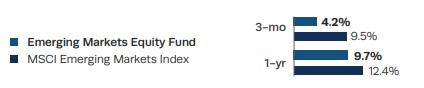

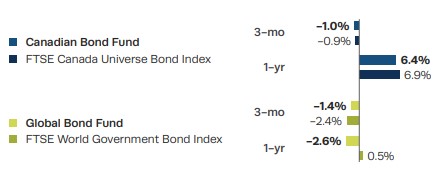

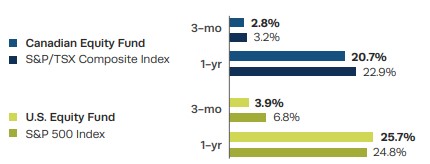

Performance has been presented for the A-Series Mawer Mutual Funds in Canadian dollars and calculated net of fees for the 3 month period of October 1 – December 31, 2019, and 1 year.

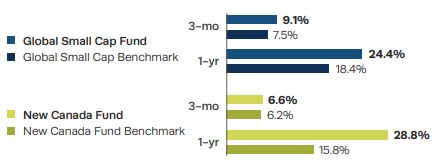

Our small-cap strategies had strong years versus their benchmarks, capped off by solid returns in the fourth quarter with many of our top-weighted positions delivering stellar returns (Boyd Group, Enghouse, Softcat, Bechtle, Diploma). Of note, investors had a euphoric reaction to results released by contact centre management software provider Enghouse during the quarter. The results provided evidence for one of the critical elements of our investment thesis: a management team that can allocate capital effectively.

Enghouse invested in a new ERP system two years ago that they claimed would allow them to integrate acquisitions more effectively. Sure enough, after having recently acquired two sizable but unprofitable software businesses, Enghouse reported that they had raised EBITDA margins in both businesses close to the company average of 31% in less than a year—an impressive achievement.

Value-added resellers Softcat and Bechtle also delivered strong results and growth predicated on their clients’ need for help in navigating increasingly complex IT and security requirements. These are business models we like, in part because they are capital-light. We generally try to avoid tech companies that compete by throwing capital at problems in favour of those that deliver advice. Though we have been trimming them to manage their weights, Softcat and Bechtle remain top holdings in our global small cap strategy, and we have added a number of IT consulting firms over the past six months to our other portfolios (Accenture, CGI, Nomura Research Institute).