President's message

Happy New Year! As I think back on 2021, I must admit I’m experiencing a bit of déjà vu. I, like all of you, had hoped that 2021 would have brought us closer to the end of the pandemic, however, the year continued to reflect many of the same themes as 2020: remote work, virtual events, COVID-19 variants, and market volatility. Despite these challenges, I’m very proud of our Mawer team—we have consistently shown resilience, adaptability, and an ongoing commitment to consistently do the right things for our clients.

During 2021, we had an extremely active year:

- We welcomed 40 employees to the firmWe welcomed 40 employees to the firm

- We launched the Mawer U.S. Mid Cap Equity Fund

- We had seven team members become new owners of the firm

- Our virtual Mawer Insight event in November hosted well over 1,000 attendees and our Art of Boring podcast will be posting its 100th episode in January!

- We hosted our first virtual Client Appreciation Event in celebration of resilience: hosted by Dave Kelly and featuring guests Angela Duckworth, Andy Kim, and Waneek Horn-Miller

- We ramped up initiatives within our Counsel for Diversity and Inclusion and continued our membership in the North American chapter of the Diversity Project

- We made significant investments in technology and automation that helped lead to a redesigned client portal, thereby lowering our operating risks

- We created a leadership development program and employee career cycle including a learning stipend for each employee to further support employee growth and firm succession planning

- We started construction on a new Toronto office location which will be completed in 2022

- And we made significant contributions back to our communities—providing over $2.8 million dollars of support across 211 different charitable organizations

Our investment performance continued to be strong over 2021 and to underscore our commitment to long-term performance, the Mawer Balanced Fund was recognized for 10-year performance (Global Neutral Balanced) by the Refinitiv Lipper Fund Awards out of a total of 93 competing funds.

Finally, I would like to thank those who took the time to complete our annual client survey. We appreciate seeing the continued strong client satisfaction results particularly as it relates to client service and overall fund performance. We also recognize there is an increasing desire to return to in-person meetings (and client events), and to continue focusing on educational topics.

On behalf of everyone at Mawer, I thank you for your continued support, and wish you all a safe and prosperous 2022.

Sincerely,

Craig Senyk, President, Vice Chair

Market overview

Global equity markets performed strongly in the fourth quarter of 2021, as generally strong company earnings releases outweighed any market nervousness over the potential accelerated tightening of monetary policy. An exception was emerging markets, which continued to face headwinds in China related to regulatory changes and imbalances in the property market (heavily indebted property developers). Canadian bonds also finished the quarter with positive returns.

There was no shortage of volatility in the quarter as market participants navigated risks from inflation pressures, supply chain disruptions, high energy prices, and central bank tapering. The emergence of the COVID-19 Omicron variant initially led to some caution, as investors sought to understand the severity and potential government response, though by the end of 2021, the impact on global markets was ultimately subdued. Overall, it was an excellent year for developed market equities as the recovery of the economy drove investor enthusiasm.

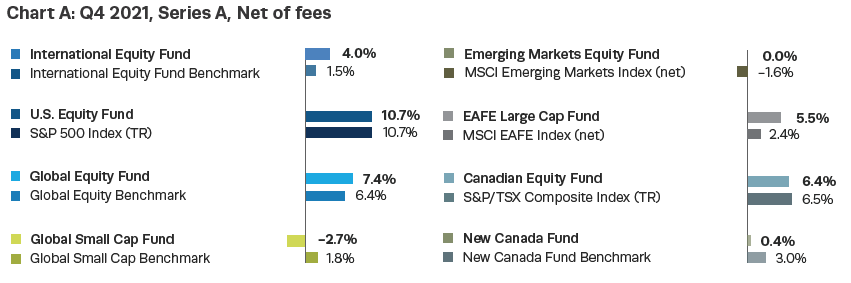

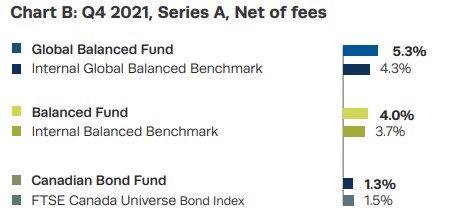

How did we do?

Performance has been presented for the O-Series Mawer Mutual Funds in Canadian dollars and calculated gross of fees for the 3-month period of October 1 – December 31, 2021.