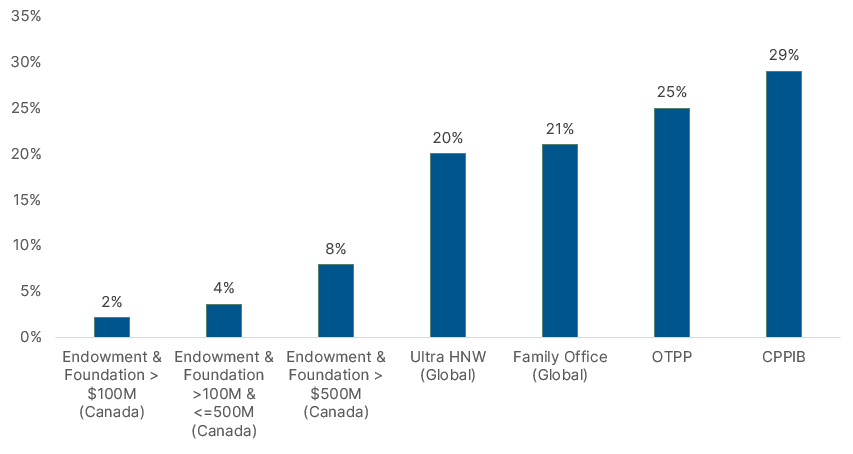

In Canada, the Canada Pension Plan Investment Board (CPPIB) has been an industry leader in building a diversified, global private equity program through a combination of primary fund, direct, co-investment, and secondary allocations, managed both in-house and externally.

Until recently, individual investors had little direct access to private equity, regardless of their investment objectives or risk tolerance. However, through innovations in fund structures, private equity is becoming increasingly accessible to high-net-worth investors.

The Honest Trade-offs

Private equity is not the right asset for every investor or every portfolio. The trade-offs are real and are worth stating plainly:

- Illiquidity is the most significant trade-off. Private equity investments are meant to be held for years, and the ability to exit early is limited. For investors with long-term goals, however, this may be a risk they’re well-positioned to bear, as longer holding periods naturally align with long-term investment objectives.

- Complexity is inherent. Private markets lack the transparency of public ones, and valuations are less frequent and less precise. Understanding what you own and how it’s performing requires more engagement than monitoring a public equity fund.

- Capital risk exists in any equity investment, and more acutely in private equity. Early-stage, venture capital-backed companies carry a higher probability of loss, and even buyout strategies, which target mature businesses, are not immune to deterioration.

- Leverage, particularly in buyout strategies, amplifies both gains and losses. It’s a tool, not a guarantee, and investors need to understand how it’s being used in any fund they consider.

None of these trade-offs are reasons to avoid the asset class, but they do mean private equity should be approached thoughtfully, with a clear-eyed understanding of what you’re accepting and what you’re gaining. For investors with the right time horizon, liquidity position, and risk tolerance, the potential benefits may outweigh the complexity.

The Question Worth Asking, And Answering

The days of private equity being exclusively reserved for the largest institutions are over.

The structural innovations that have made it more accessible are meaningful, and the case for including it in a long-term portfolio, as part of a thoughtfully constructed allocation, is well-founded.

For most high-net-worth investors, the question isn’t “does private equity belongs in my portfolio”? It’s “do I have access to it through the right managers, in the right structure, at a fee level that leaves enough of the return premium to make the complexity worthwhile”?

This question is worth examining carefully, and it begins with understanding why not all private equity is created equal.

Keep an eye out for the next in this series, How to Access Private Equity: Manager Selection, Structure, and Fees, to learn more.